Why China is still buying gold

While western investors are dithering and selling gold and silver for fear they might go lower, China is buying up all available bullion. Record export earnings make it inevitable.

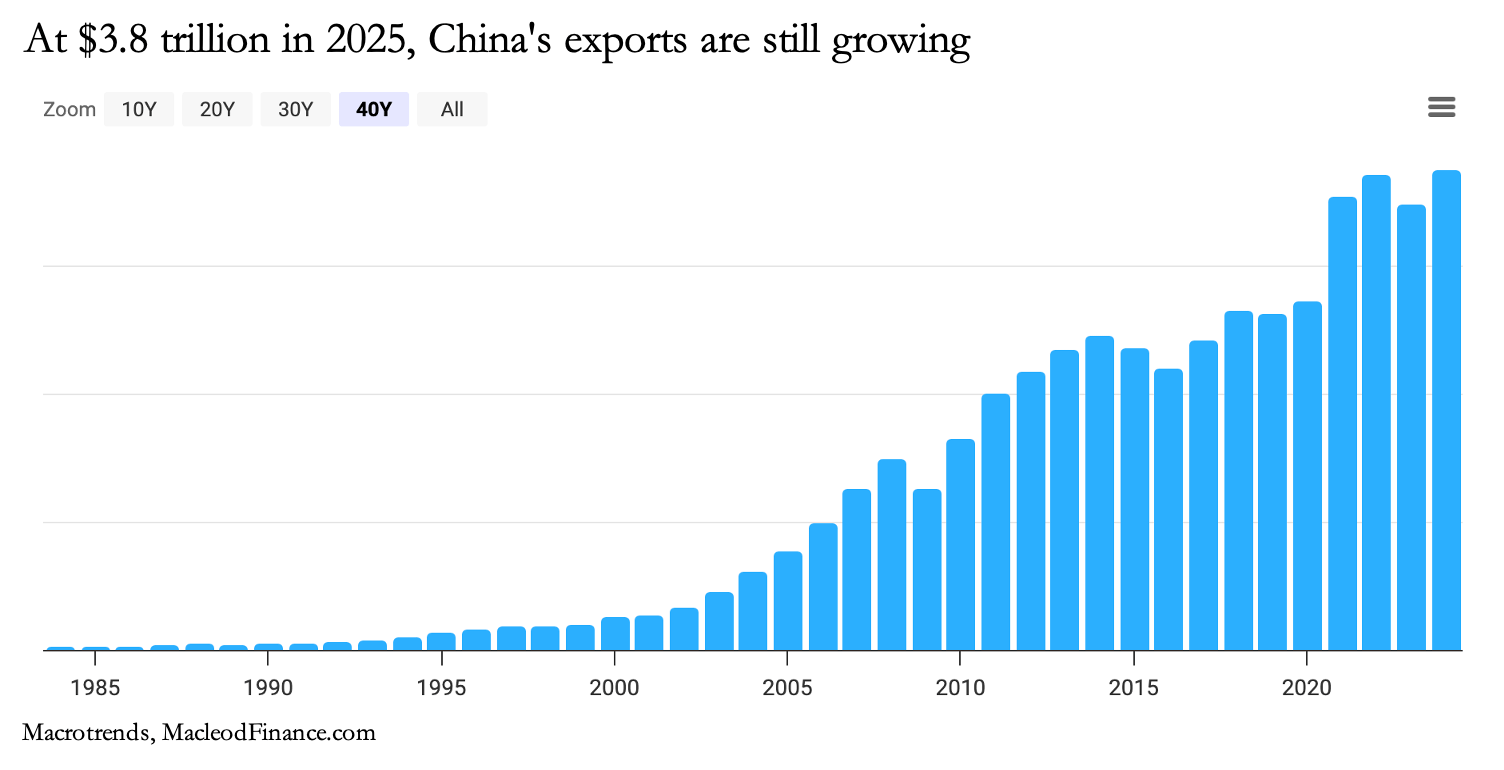

China has a surplus dollar problem:

Introduction

Today, China’s export surpluses are larger than ever giving the PBOC an unwanted dollar headache. She has little need for other G7 currencies and their debt, so they can only be sold for precious metals. This is confirmed in the gold and silver import statistics for China in what we know of them in 2026 so far.

It was a problem anticipated by the post-Mao administration as they planned their way into capitalism, unleashing enormous economic development coupled with a high consumer saving mentality. Ever since then, China has had the problem of excess dollars, and it is still growing. But the communist party understood from the outset the danger of being hostage to a rival national currency.

Back in 1983, China’s communist party appointed the Peoples Bank (PBOC) with sole responsibility for buying and selling gold and silver. It was logical, because the PBOC was also the monopoly dealer in foreign exchange. And while I’ve told the story many times about how the PBOC accumulated an estimated 20,000 tonnes of gold before setting up the Shanghai Gold Exchange in 2002 and permitted the general public to buy gold from then on, the silver story has been neglected. But it is a tandem operation. I shall release an analysis of China’s silver policy in a separate article.

Gold mining developed deliberately with China becoming the largest mining nation almost from scratch. From only 50 tonnes in the early eighties, rising to 100 tonnes in the early nineties, and overtaking South Africa in 2007, China has mined an estimated 10,200 tonnes by the start of this year. Virtually no gold leaves China, so what the Chinese mine and buy is locked away from global markets.

Estimates of gold imports since 2002 vary widely between 15,000 —25,000 tonnes. Deliveries from SGE vaults post-2002 into public hands total over 28,000 tonnes, some of which will have been scrapped and resubmitted to the government for refining.

However, this does not include gold designated as monetary. If the PBOC buys gold from another central bank, or books it as monetary it goes unrecorded in China’s import figures. Investor uncertainty in Europe and North America doesn’t faze the Chinese either, who continue to sell dollars in favour of gold having bought an estimated 473 tonnes of non-monetary gold so far this year to end-April. That’s a run-rate of nearly 1,500 tonnes annualised, selling nearly $70bn so far.