UK bonds crisis ahead

Foreign hedge fund investment, one-third in inflation linkers, and a socialist government destroying the tax base combine to make the UK gilt market and sterling a potential disaster.

Introduction

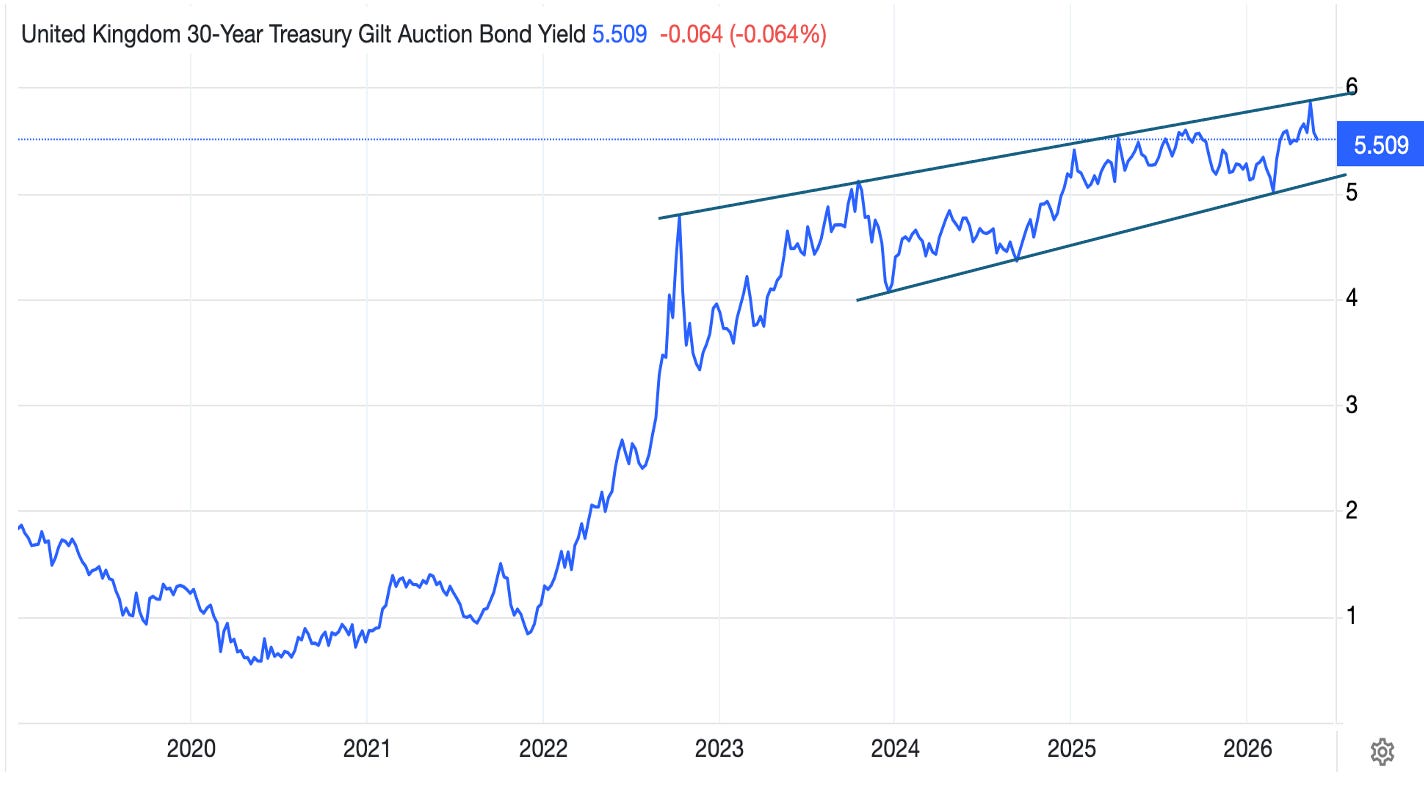

Any technical analyst will tell you that when the yield on the long gilt (illustrated below) breaks above the 4-year upward sloping channel, it will rise strongly. The minimum arithmetic projection is to 11%, while the logarithmic is 22%.

Similar readings are evident in all G7 currencies. The link is with their purchasing powers, which can now be expected to decline at an accelerating rate. This was less obvious to financial markets before the Iran war, but nevertheless the trend with the entire commodity complex being in a bull market was established in 2020, showing that the major move to higher bond yields correlated with the commodity bull, which initially peaked in mid-2022.

Since May 2025, long before the war on Iran kicked off commodities began their current run only just surpassing the May 2022 highs so far. The closure of Hormuz and its knock-on effects have only brought forward commodity price rises and not created a new trend. Clearly, the commodity bull has a long way to go, which brings us back to the relationship with bond yields.

As a matter of plain fact, a commodity bull market is evidence of a fall in currency purchasing power, conventionally recorded as inflation when it works through to consumer prices. Bond markets will reflect this fall in purchasing power through higher yields. And when investors expect a further decline in purchasing power for a currency, they will only invest in government bonds which offers them compensation for the risk of falling purchasing power. This is why both bond yields and commodities rose together between 2020—2022.