Summer doldrums

Over the last six months, gold and silver are barely changed. Investors are losing patience. It’s time to stand back and examine the big picture and ignore short-term sentiment.

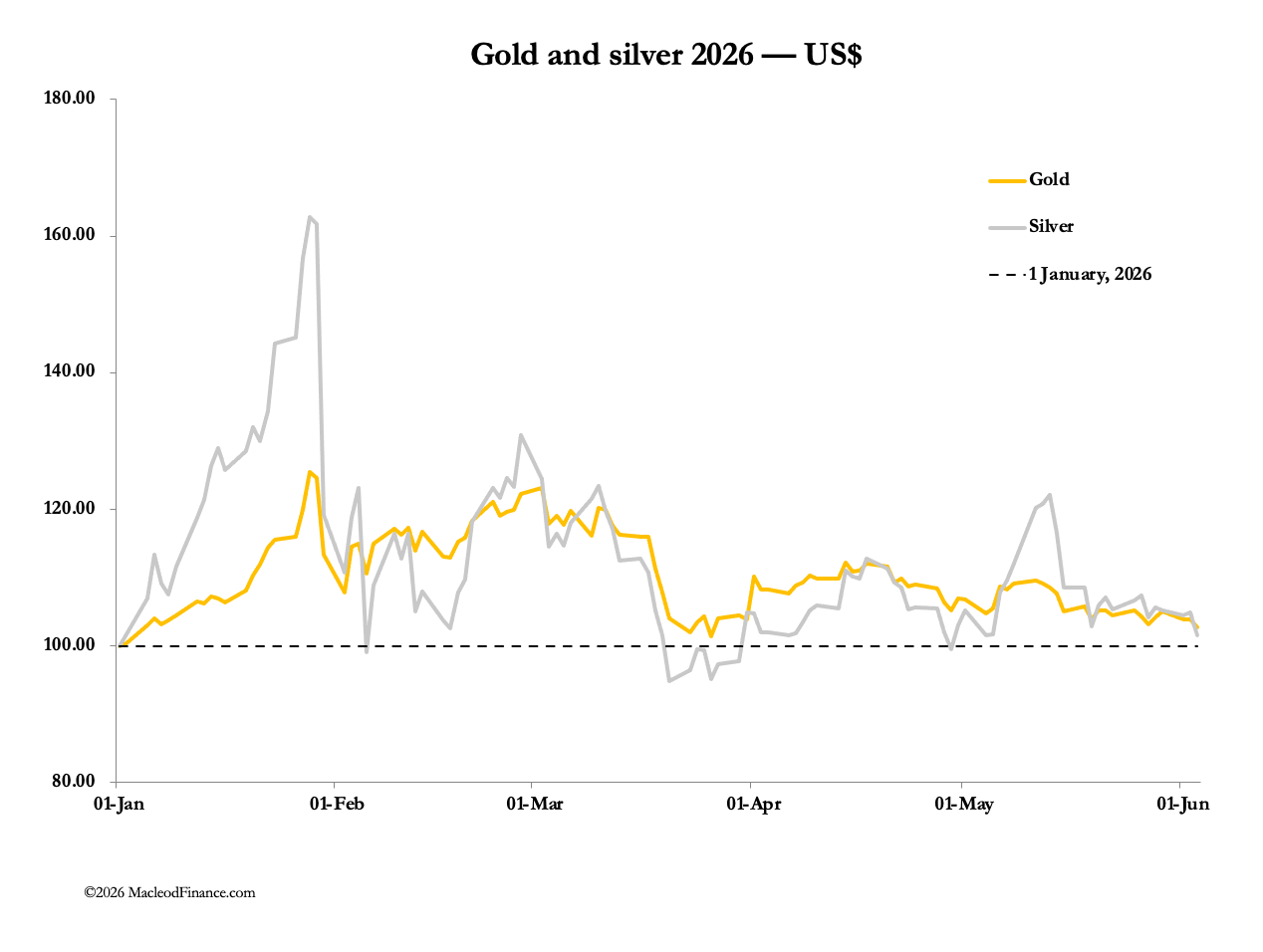

As our introductory chart shows, gold and silver are barely changed on the year. As a measure of investor sentiment, North American investors sold down 12 tonnes in gold ETFs in the last two weeks of May, according to The World Gold Council. Doubtless, this week they sold some more.

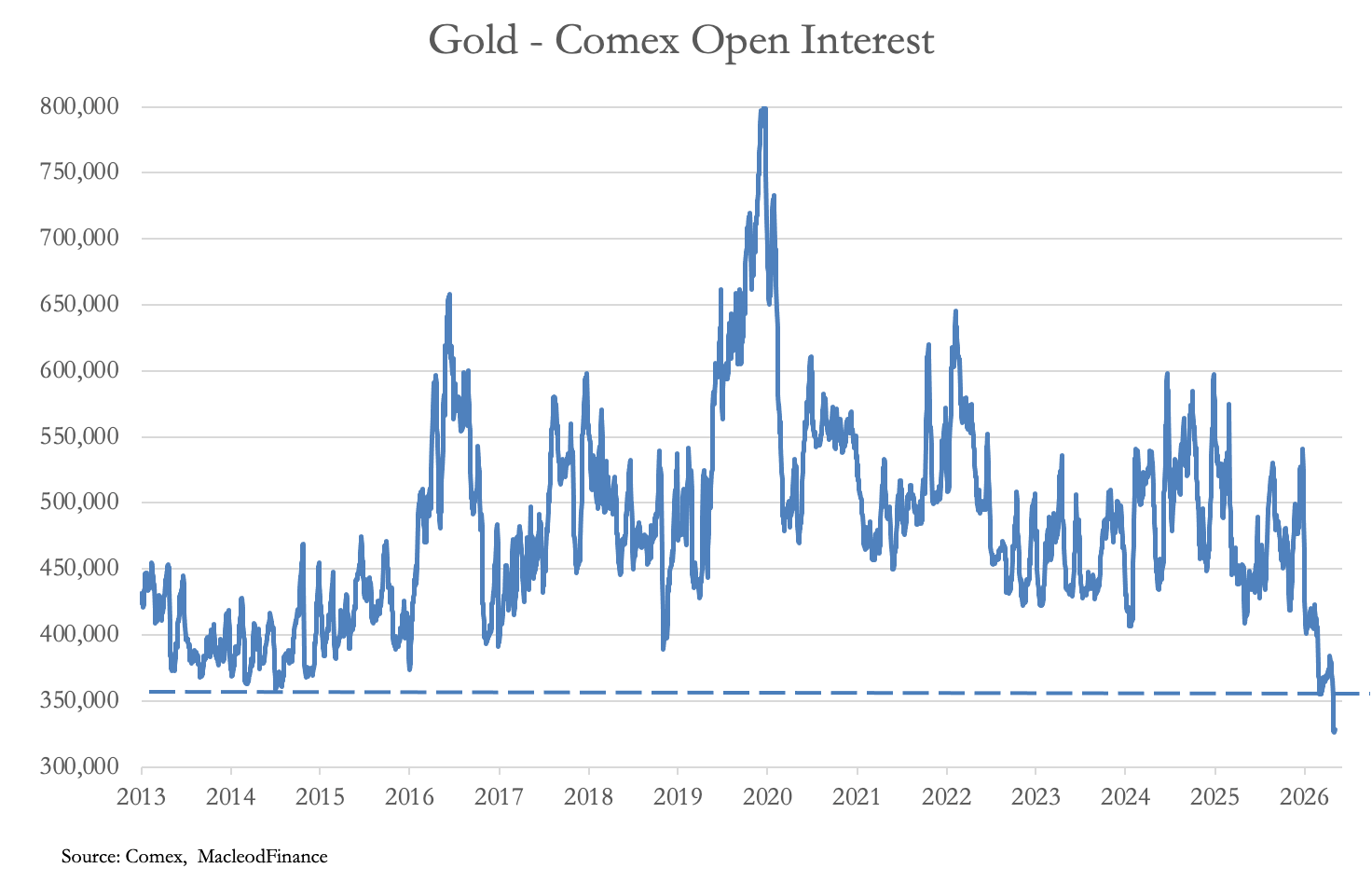

This is one proxy for market sentiment. This disinterest is also reflected in open interest on Comex, which has collapsed to the lowest levels for decades, even lower than at the end of the 2011—2016 bear market when sentiment was extremely negative, and from which the current bull market commenced:

Mood swings in markets always lead investors to buying tops and selling bottoms. Market makers know this and exploit investor sentiment ruthlessly. The time to kick an investor hard is when he is down. This is why very few people trade successfully and consistently.

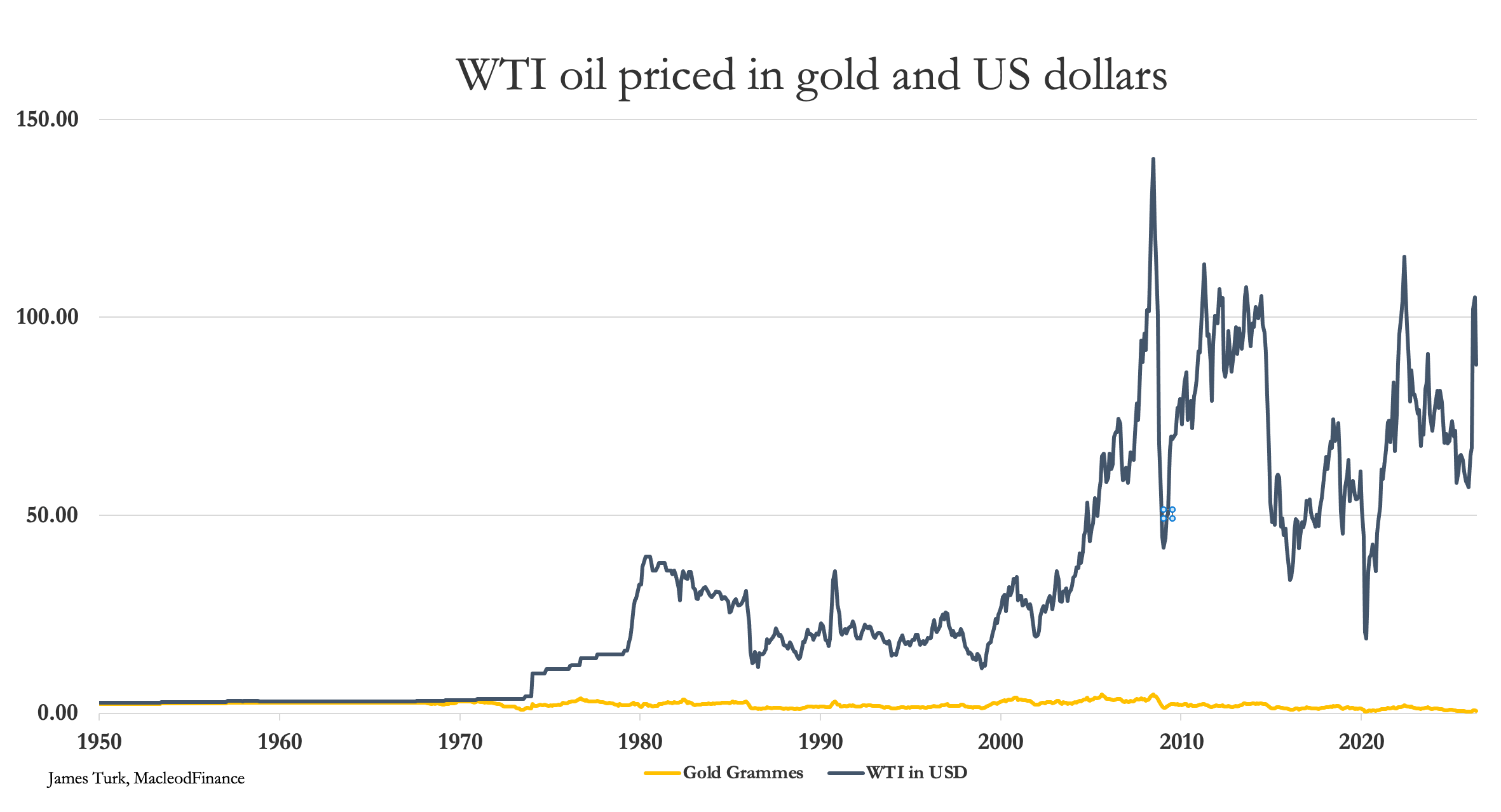

In horse racing, the bookies make lots of money at the expense of the punters. It’s just the same in financial markets. This is why at MacleodFinance we discourage trading gold, insisting on stacking in the knowledge that the risk is in currencies and credit and not gold. Gold is legal money without counterparty risk, and has been remarkably stable in its purchasing power over long periods, as the next chart of the oil price in gold and US dollars demonstrates:

Currently, oil priced in gold is trading at a 40% discount to its stable post-war 1950—1972 Bretton Woods level, whereas in fiat dollars it has risen 25 times with great volatility along the way. This story is repeated for all commodities, reflecting the dollar’s loss of purchasing power, which is now accelerating, made increasingly obvious by the Iran war.

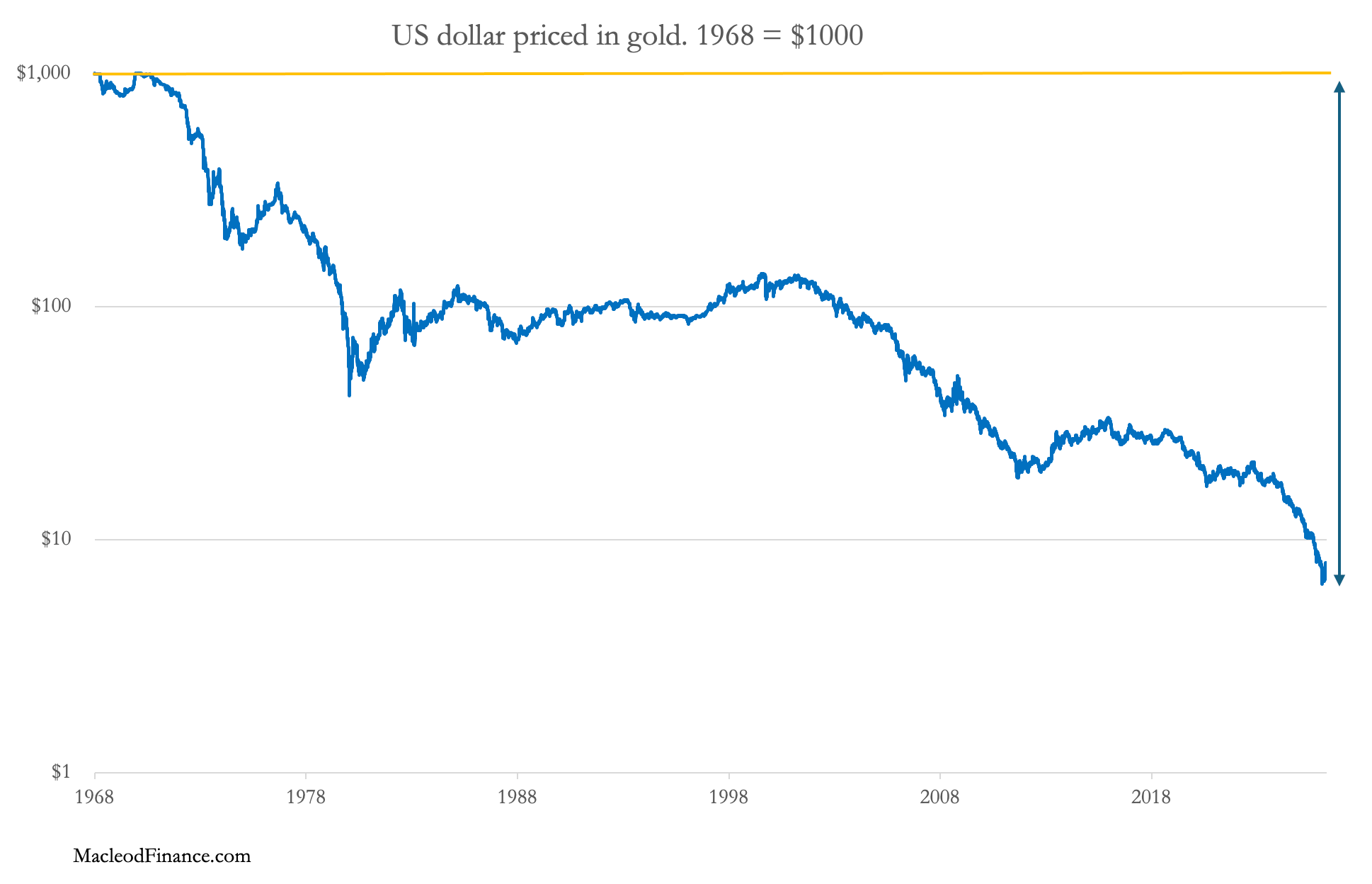

Would you rather have gold, which in times of currency stress is stable, or the fiat dollar with its inherent weaknesses? This is what the dollar is doing relative to gold:

If you had $1000 in cash in the late-1960s, it would have lost $994 of its purchasing power by now. Furthermore, the rate of this loss is demonstrably accelerating.

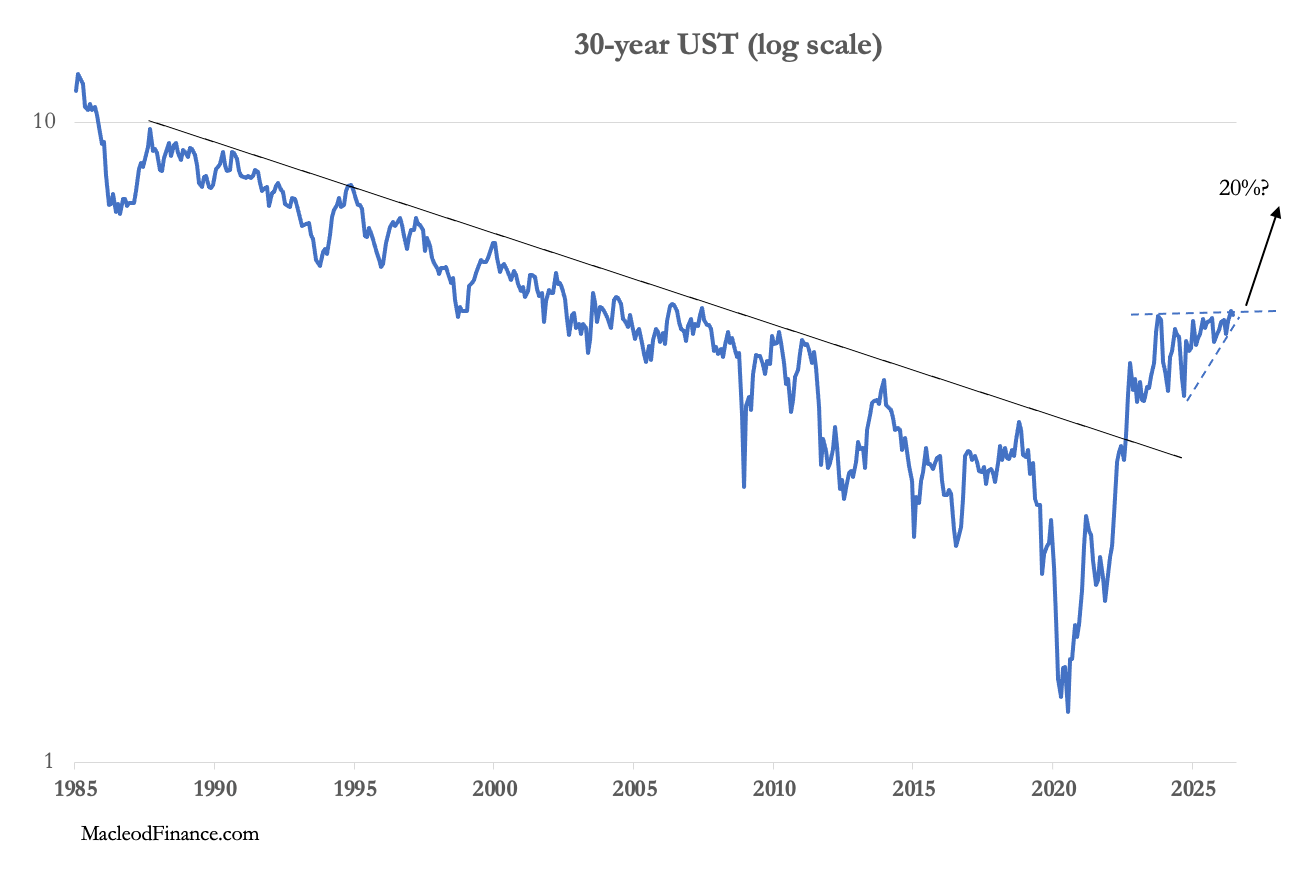

The current gold/dollar exchange rate is irrelevant when fundamental factors are leading to a renewed loss of purchasing power for the dollar, misleadingly reported as price inflation. The Gulf war is bringing on the crisis, leading with certainly to an economic slump and rising prices. This is certain to reduce all G7 government revenues while at the same time increasing their spending commitments. From a debt-to-GDP starting point averaging about 120% on average, not only are bond yields set to rise significantly, but G7 government debt will simply become unfundable. Our next chart shows that the US long bond yield is on the verge of breaking higher, with disastrous consequences for financial assets and the dollar itself:

You would think that common sense will intervene and prevent this outcome. But that ignores a simple fact: economic outcomes are driven by politics, not sound economics and certainly not common sense.

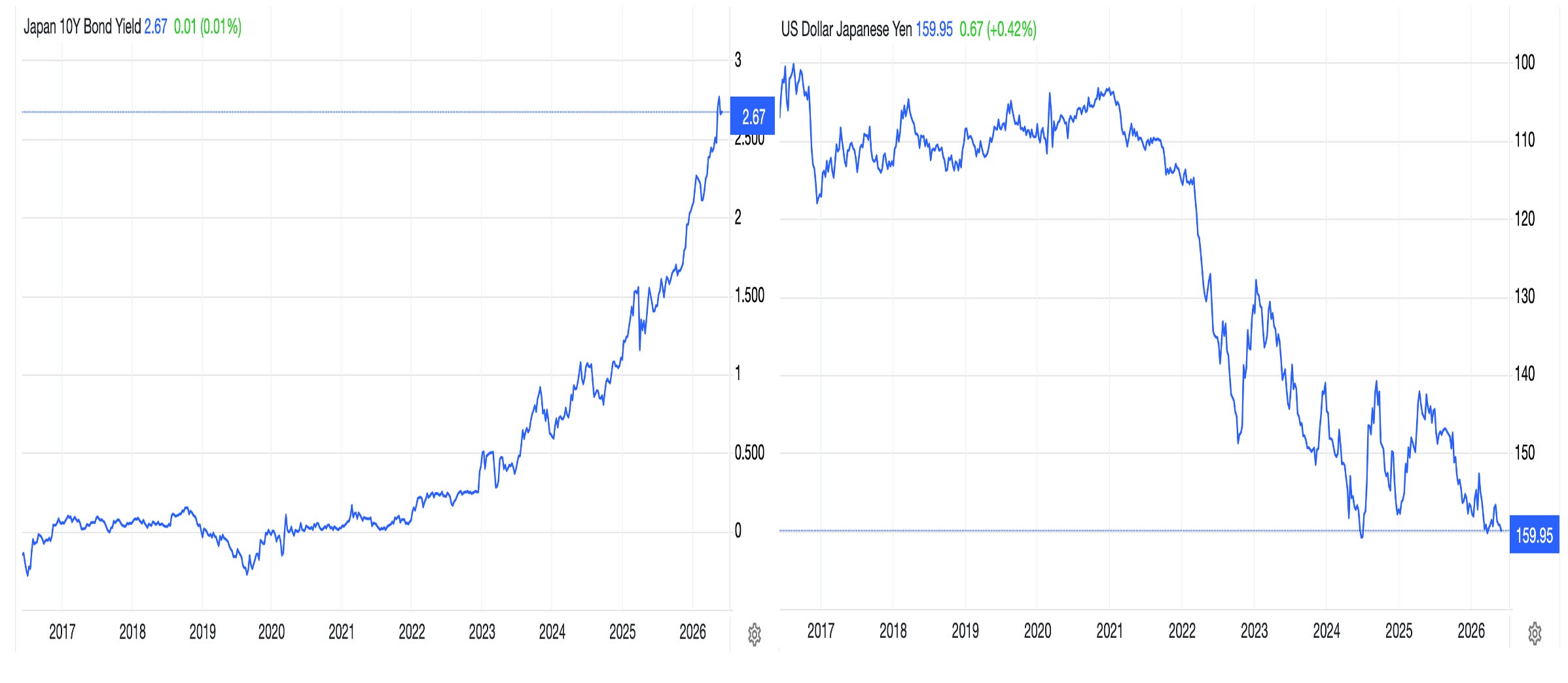

Take Japan. Its prime minister thinks she can defend the yen by increasing spending in an attempt to strengthen the economy. In other words, she is having a Liz Truss moment but with a debt to GDP of 250%. And Japan depends almost entirely on imported oil and gas as well as fertilisers etc.

Doubtless, the Bank of Japan is furiously defending the currency against this madness, which is challenging all-time lows, while bond yields are soaring:

Last time this happened, which followed the oil crisis of October 1973, Japan’s CPI inflation rate soared to 25% by spring 1974, while the wholesale price index rose nearly 35%. The situation for Japan today certainly rhymes with 1973—1974. And being the largest source of foreign investment capital for the US and the rest of the world, the inevitable crisis Japan faces will affect us all, particularly the US government because Japan is the largest foreign holder of US treasuries.

In conclusion, current investor sentiment obscures the brutal facts facing the fiat currency world. Anyone who gets upset about losing money day-to-day by holding gold is suffering from extreme myopia and is prey to the real professionals such as central banks and market-makers who play on investor sentiment to get you to sell your gold to them.

Hold Fast!

Jesse Livermore once said the big money comes from sitting tight.

Gold's been on a wild multi-year run, smashing all-time highs earlier this year before pulling back to the mid-$4,460s on some short-term profit taking.

But the bigger picture hasn't changed-central banks keep stacking, geopolitics are messy, and safe-haven demand is strong.

Plenty of analysts are still calling for $5,000-$6,000+ by year-end.

Once you're positioned right in a real trend, the key is patience. Let the winners run. Big moves don't happen overnight, and trying to dance in and out usually just kills your profits.

Sitting tight on gold here. You?

Central banks run the world. Central banks are buying gold. Be your own central bank. Buy gold.