March futures expiry

It’s clear that as the Iran war rages, the dollar will be a casualty and gold benefits. But the bullion banks need to square their books. That’s what contract expiry is currently all about.

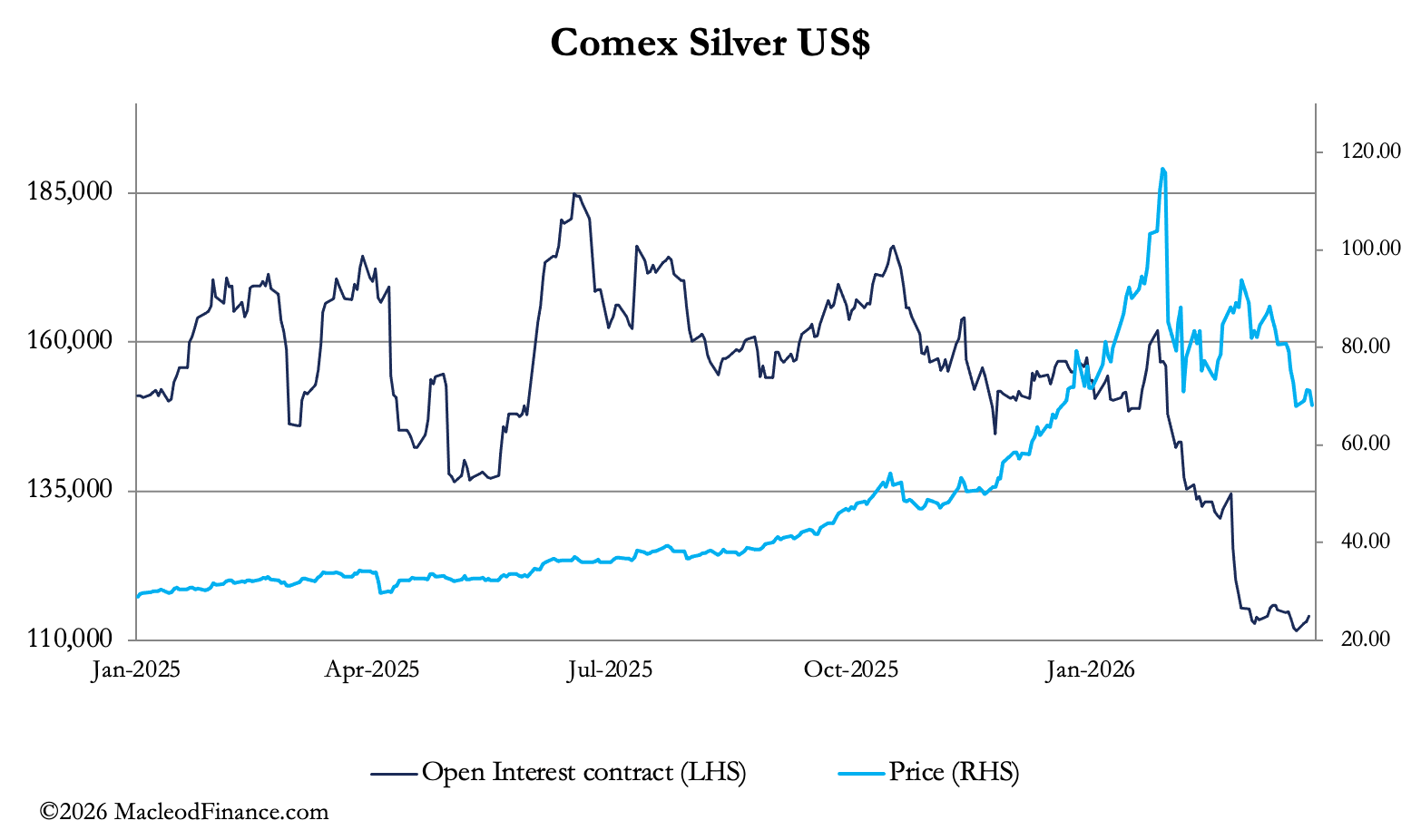

Looking at the silver chart below, it may be too early to call a resumption of the bull trend but coupled with the lowest open interest for over 20 years, one can only conclude that paper silver is deeply oversold and will struggle to go any lower. Furthermore, when it does turn, it’s set up for a massive run higher given a severe lack of physical and that despite prices almost halving backwardations persist. Gold is similarly oversold with Comex open interest under 400,000.

This week saw further weakness in gold and silver prices. In European morning trade today, gold was $4410, down $55 from last Friday’s close having hit a low on Wednesday of $4100 approaching its 250-day moving average. Silver at $68.20 is up 30 cents net, after testing $61. Turnover in both Comex future contracts was reasonably high.

Yesterday was the last trade day for April’s Comex options. This explains the heavy mark-downs as bullion traders who had sold calls were incentivised to ensure as many as possible would expire worthless. This is followed by the expiry of the April contract with the start of the 3-day delivery process commencing next Monday.

The April contract is the active one for gold, and on preliminary figures last night there were still 63,034 contracts to sell, roll, or stand for delivery. Silver is relatively unaffected, its next active contract being May. But in gold’s case, we cannot rule out paper shenanigans until All Fools Day next week

In previous market reports, we have pointed out that gold is driven less so in war as a safe haven than the dollar. For liquidity, regulatory, and accounting purposes the dollar is preferred, and this is reflected in the chart for its trade weighted index: