Inflation undermines all asset values

The febrile condition of all asset markets headed by rising G7 bond yields is leading to uncertainty for gold and silver prices. One last sell-off is a golden opportunity for stackers.

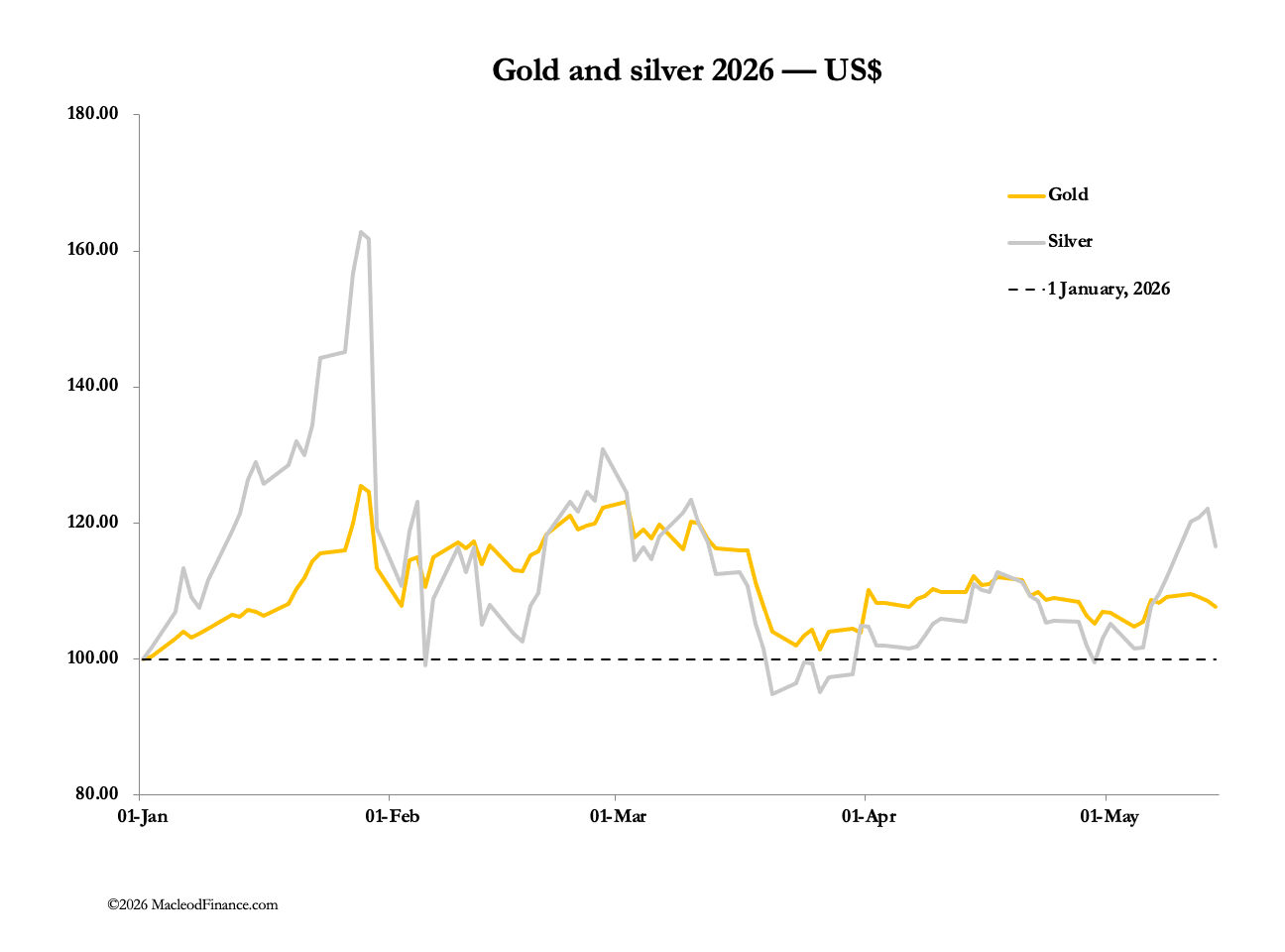

For the first half of this week, gold and particularly silver prices rose before being hammered yesterday and this morning. In overnight Asian trade, gold was $4582, down $95 from last Friday’s close, and silver at $79.20 was down $1.00. A 16,556 jump in gold’s preliminary open interest on Comex yesterday suggests active shorting by hedge funds, while open interest in silver declined by 2,270 confirming that it was gold/$ pair traders in action.

While preliminary open interest figures see some revision before being final, this selling when gold’s contract is already oversold is consistent with a final sell-off. The swaps, being mainly market makers and bullion bank trading desks which take the short side will be delighted, because they know from the quality of buying both in New York and London that they must try to achieve and maintain level books.

This sudden bearishness on the part of hedge fund traders is linked to this week’s inflation shock, with April’s accelerating to 3.8% from March’s 3.3% driven mainly by energy costs. That this should prove a shock is an indictment of sleepy markets, but traders have now been alerted to the severe consequences of oil prices rising and US reserves depleting.

Bond yields are rising in sympathy, as the chart of the US 10-year treasury note shows:

The yield is rising to test and potentially break out above the post-covid rise in yields (the upper pecked line). The long-term chart puts this in context. When yields break higher, they have the potential to at least double from current levels: