Gulf war and gold

In the fog of war, truth is the casualty. Gold and silver prices will reflect uncertainty over outcomes. All that traders know for now is that bond yields might rise further.

Well-informed analysts who follow geopolitical developments have concluded that America and Israel have lost the war against Iran, and Hormuz will remain closed. But investors are driven by sentiment, which is basically their reading of past market trends relative to current prices. Never has the gulf between the two assessments been greater. We discuss this divergence, the reasons behind it, and the probable outcome for markets, and in particular for gold and silver.

There are two interrelated facts which must be noted. The first is that the US/Israeli attempt to destabilise Iran has failed, and consequently Hormuz will remain shut for the foreseeable future. And the most recent evidence is that Iran is increasing the pressure on the US by renewing attacks on their assets in the Gulf. Furthermore, there are early signs that the Houthis in Yemen will get more actively involved and assist Iran by closing the Bab al-Mandab strait to shipping, restricting oil exports from the Saudi terminal at Yanbo.

Despite the fog of war, we can be certain that the effective elimination from global markets of 15 million barrels a day of crude and condensate plus a further 5 mb/d of refined petroleum products such as diesel and jet fuel will impact prices with shortages driving them higher. In addition, global shortages of fertilisers, sulphuric acid, and helium to mention just a few oil derivatives will have their impact. China’s response has been to protect her economy by stopping fertiliser and sulphuric acid exports, further tightening global supplies.

The second fact can be discerned from China’s policies via-a-vis the US dollar, which it has been dumping as rapidly as possible. Being closely involved with Iran, China’s intelligence appears to conform with what independent intelligence analysts tell us: that Iran has won the war and is out to destroy the US presence and her relationships with GCC members in the Middle East. Consequently, the dollar is losing credibility, which is why China is selling them and establishing a global gold trading facility in Hong Kong.

China expects nothing less than the death not only of the petrodollar, but of the fiat dollar itself.

Investors in western capital markets have been broadly oblivious to these developments. But with renewed Iranian attacks and increasing bellicosity from the US administration, there is no doubt that this is beginning to affect bond markets.

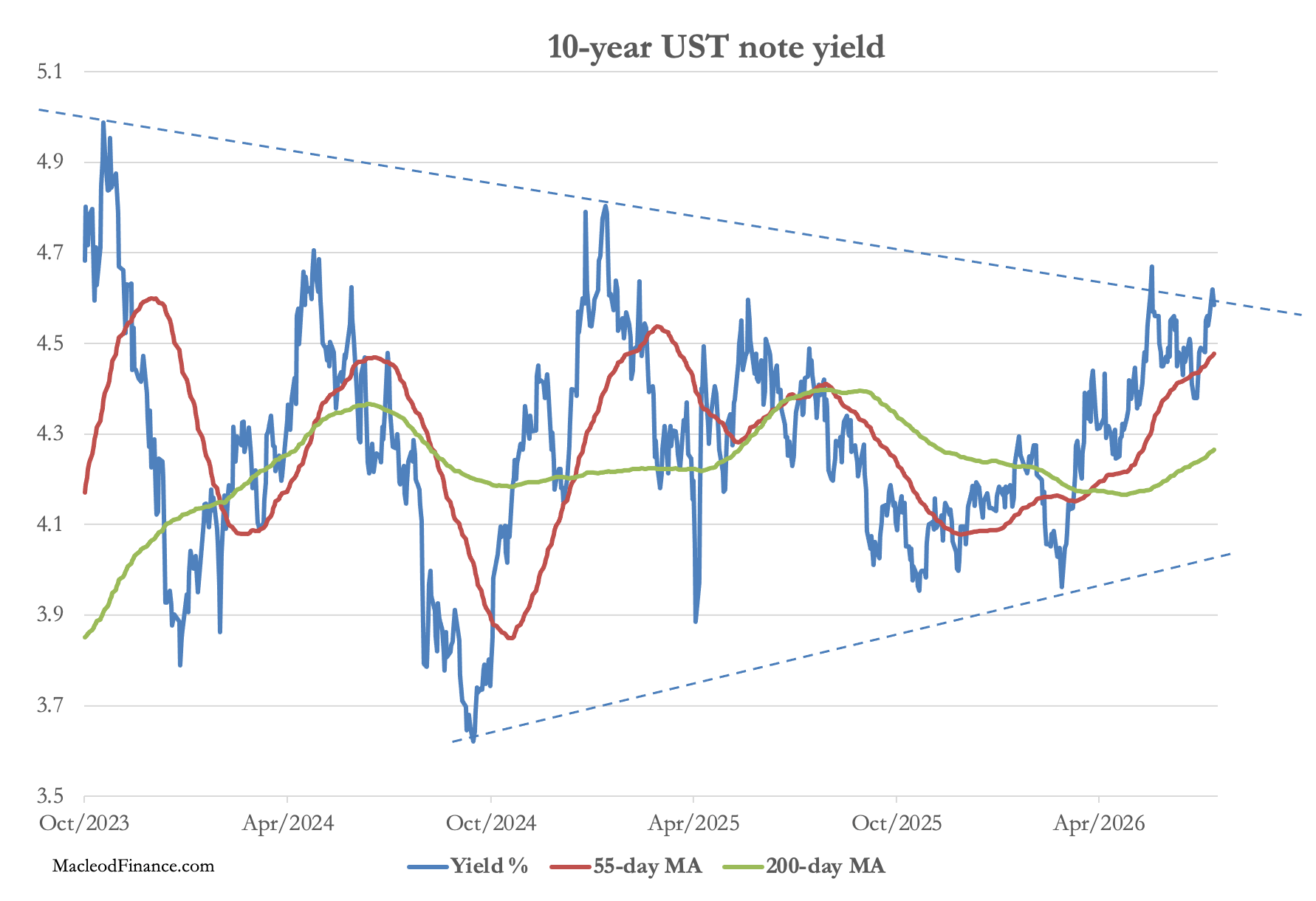

Today’s markets are driven by sentiment and not fundamentals. This is to be expected in a credit bubble where greed dominates over caution. For decades, investors have increasingly turned to charts in the way Romans examined entrails of goats to predict the future. It is easier than trying to think things through. Technical analysis is valuable for discerning sentiment and trends, but they are right until suddenly they are not.

This is the chart which is now worrying investors:

Conventional technical analysis indicates that the yield on the 10-year US treasury note is in an uptrend, also apparent in most of the other G7 bond markets. Furthermore, there are signs that the yield is breaking out above a three-year consolidation pattern. The next chart puts the importance of a breakout into context.