Collapsing currencies

Consumer prices face a new round of increases. They will be far greater than anyone expects because they will be the consequence of the US dollar and other G7 currencies failing.

It is clear that investors are clueless over what’s about to hit them. Surprises will include bond yields rising significantly, bursting the equity bubble. Only then will they discover that “inflation” is going off the charts. Inflation is an inaccurate definition of the malady; it is actually currency purchasing power declining — potentially catastrophically.

In the interests of alerting as many MacleodFinance free subscribers as possible to the dangers to their wealth along with anyone to whom it might be forwarded, this article is free to share, and you are encouraged to do so.

Introduction

We can now see what a disaster the Iran war is with respect to the supply of energy and downstream products, such as sulphur, sulphuric acid, sulphates, and helium to name just a few. Furthermore, other exporters of these essentials are restricting their supplies into global markets to protect their own industries. Higher prices due to supply constraints are bound to follow affecting all goods and services, and we need to understand the consequences with clarity.

So ingrained are false narratives about inflation, that what actually drives changes in a currency’s purchasing power needs explaining. The key point is that macroeconomic analysis fails by being mathematical to the exclusion of changes in human preferences.

The first argument to grasp is that a medium of exchange, such as the dollar currency, is a commodity the same as any good or service with a price. Just as the price of a commodity depends on the sum of individual demands in the context of the supply available, the same is true of a currency. This differs from macro-monetary analysis which only assumes that additional currency supply from the issuer will lead to a decline in purchasing power of the currency unit. This may well happen, but it is not a simple matter of a proportional effect.

Putting the matter in the context of human preferences gives a far better understanding of why a currency’s purchasing power alters. If we assume for a moment that there is no increase or decrease in the currency quantity or the supply of a range of goods, then it is changes in aggregate consumer preferences for or against possessing the currency which will alter its “price” or purchasing power.

Nowadays, we are not only considering a consumer’s cash in the form of banknotes, but the currency resources he has at his disposal in the banking system: current and deposit accounts, overdraft facilities, other liquid savings, and credit cards. Now, let’s assume that our consumer happens to like beans and wants to buy more. He has a simple choice. He can reduce his purchases of other items to release funds to buy more beans, or he can draw on his cash facilities to pay the price.

If he decides to draw on his currency balances to pay for the beans or any other consumer good, he exhibits a preference for them over cash. If, as is likely to be the case, our consumer in common with a significant number of others decides to draw down on their currency balances, then the “price” or value of the currency will decline, undermining its purchasing power, while the values of the goods bought in exchange will increase due to the extra demand. It follows that if a majority of consumers act in this way, that the purchasing power of the currency will fall, potentially significantly.

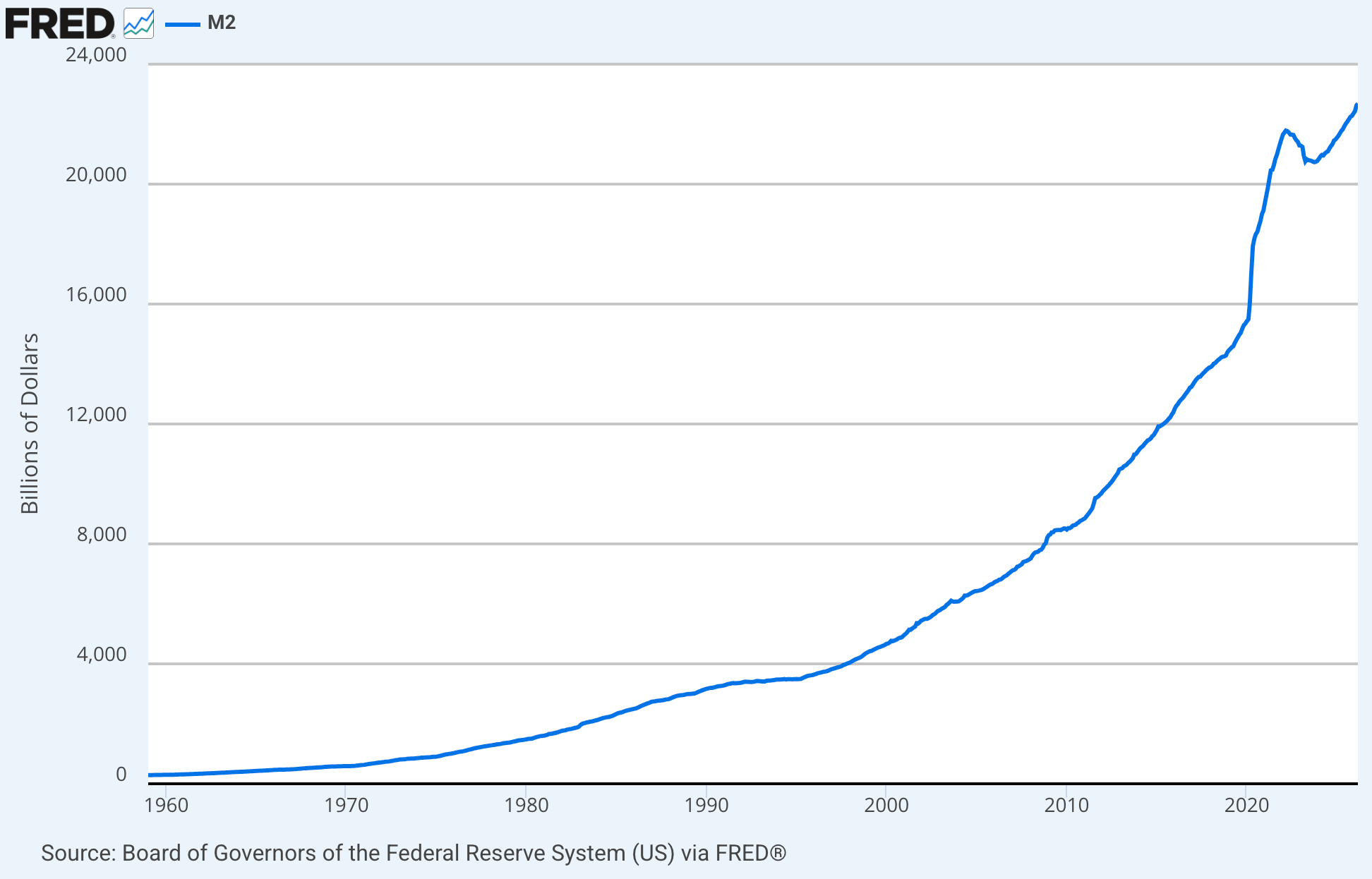

So far, we have not considered price effects if the quantity of currency is expanded or contracted, only if it does not alter. But the quantity of currency has been expanding for a considerable time, as the chart of dollar currency supply indicates:

When the quantity of currency in circulation expands, and its expansion is matched by an increase in demand for it, then the currency will maintain its purchasing power. But if demand for the currency fails to keep pace with the increase in its quantity, then its purchasing power will decline.

We can now anticipate a combined effect, rarely predicted by the mathematical economists:

· If demand for a currency fails to match the expansion in its supply, its purchasing power will decline.

· If sufficient actors take the view that they should reduce their currency holdings in favour of goods, then not only is the currency sold, but the demand for goods increases their value, further undermining the purchasing power of the currency.

This is why changes in consumer attitudes can have a dramatic effect on a currency’s purchasing power. The effect is not to be underestimated. If all consumers begin to realise that rising prices for everything are due to the currency’s value declining, then they will dump all the currency at their disposal to buy goods — any goods indiscriminately. The currency becomes worthless, because as a commodity, no one wants it.

The Iran war and its consequences

The virtual closure of the Straits of Hormuz and the ongoing conflict between America with Israel against Iran is destroying supplies of energy and energy derivatives while disrupting shipping logistics. The production and supply of almost all goods are affected. The outcome for prices is clear. It is impractical for individuals to stop buying everything because higher prices are unaffordable. They are bound to draw down on their currency balances to acquire their necessities.

This means that they will sell currency for the goods they deem a priority, reducing the value of the currency even without the issuer inflating its supply. We repeat: the key to understanding the value effect of the currency is to know that it is a commodity being sold in preference for other commodities. Some commodities and products will see significant declines in demand due to far higher prices, perhaps with some being unobtainable. So not only will preferences disfavour currencies, but of very many goods as well.

As well as the drawdown on currency balances and even liquidation of savings reducing the value of currency, whole swathes of economic activity will see a slump in demand. A slump in economic activity undermines tax revenues, throwing government finances into chaos. Governments with welfare and other interventionist commitments will be unable to fund their increased budget deficits.

There is only one outcome: governments’ costs of funding will rise sharply, so bond yields will soar undermining the value of all financial and other assets that depend on low interest rates.

The consequences of a major disruption of the supply of all goods, and how it undermines a currency’s purchasing power has so far been described assuming the currency issuer does not expand its quantity. Even without that additional currency supply, the conditions exist for a collapse in the currency’s value driven by a flight to goods accompanied by a collapse in government finances. This is what is meant by a fiat currency’s value depending on no more than faith. That faith can evaporate even without any change in its quantity.

However, governments are bound to respond by attempting to raise their support for the economy by increasing price controls and business subsidies, all of which add to debt which is becoming unfundable.

The funding crisis commences from abroad

Essentially, G7 governments face a debt crisis where funding cannot be achieved at any level of bond yield. The higher the yield, the worse the position. The first to recognise the dilemma are foreign holders of a currency and the US dollar is particularly exposed. According to US Treasury TIC figures, Foreigners own $44.6 trillion in financial securities, including $21.2 trillion in equities and short-term deposits of $8.9 trillion. The signs of decline are already there, with these totals beginning to decline.

Furthermore, central bank and other top insiders continue to sell dollars for gold, sending a clear signal that they expect the dollar’s purchasing power to decline further. With the US Treasury relying on foreign holders to buy their debt and certainly not sell, it faces a funding crisis even without rates going higher. If the Fed fails to raise its interest rate, the dollar will simply weaken sharply priced not just in gold, but the entire commodity complex. This advance warning is already happening, as prices for gold and any basket of commodities have indicated.

It is a situation which could evolve very rapidly into a complete destruction of the dollar’s value. And where the dollar goes as a fiat currency, given that it is the international reserve currency, others will follow. The value and economic destructions will be on an unimaginable scale. The only escape is to get out of currencies early before they lose all their value. The alternative is gold, silver and storable commodities without the counterparty risk which is the defining feature of currencies.

The crazy thing about the world we are living in. The greatest country in the world is funded by all the poorer countries by force (petrodollar) and yet most citizens of this greatest country think that they do not need these peasants. A debtor rejected its creditor and think everything will be fine.

I think in the future there will be mercantilism and just in-case ism. Which means that there will be duplicate and thus more commodities will be required compare to the previous world we know when everyone shares.

Interesting summary Alistair. I am comfortable with my physical gold/silver positions. If the stock market has a serious correction or even a collapse, will gold and silver miners fall also to the same degree, or would they be potentially likely to have a more shallow correction followed by a quicker bounce?