Chinese demand is driving gold and silver

Despite continuing efforts by the paper establishment in western capital markets to shake out weak gold and silver holders, they are being swamped by Chinese physical demand.

This week has seen underlying firmness in gold and silver markets, with gold trading at $2351 in European trade this morning, up $25, and silver at $30.82, up 45 cents. Silver was especially volatile, falling sharply mid-week before rallying over 4% yesterday. Being Friday and China off for the weekend, the shorts are taking the opportunity to unwind some of yesterday’s rise.

Having had such strong rises since mid-February, technical analysts have been calling for more consolidation before a resumption of this bull phase. The position for gold is shown next:

So far, gold has reacted to find support at the 55-day moving average, but the longer-term 12-month average is still below $2100, suggesting that a deeper correction is possible. The technical chart for silver is next

Technicians would argue that the silver price is still too far above its moving averages for comfort. It would be wrong to dismiss these concerns out of hand, but there are more important forces at play.

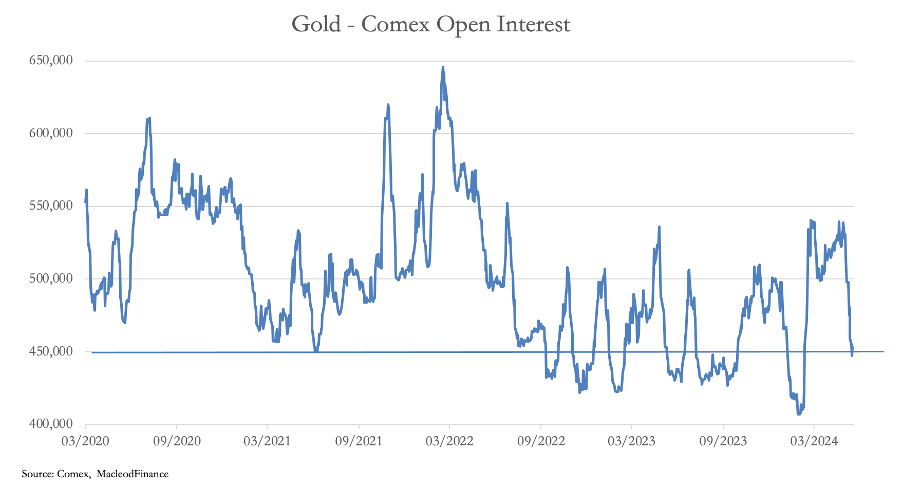

The next chart shows that gold is closer to being oversold than most analysts think:

Why have I taken Comex’s open interest as the indicator? Because it encapsulates the combined positions of all categories on Comex. The solid line at 450,000 contracts clearly indicates an oversold market, strongly suggesting that we are near to a price bottom.

But the clincher is the rate at which physical metal is draining from western vaults. According to Doug Casey’s Substack latest post, huge premiums in Shanghai are draining western vaults, with LBMA’s vaulted silver stocks falling 60% this year so far, and Comex’s falling by 46%. Gold’s drain has been less dramatic perhaps, but recent days have seen record stand-for-deliveries. In the last eight trading sessions, nearly 90 tonnes of gold have been stood for delivery taking the total so far to 253 tonnes, a rate which easily exceeds this year’s US gold mine annual output estimated by Metal Focus at 166 tonnes.

In previous postings, I have pointed out that it is massive Chinese household savings with unattractive alternatives driving demand, and this was evidenced yesterday (Thursday). Changing the pattern of recent trading sessions, gold and silver prices opened higher indicating overnight demand had returned. It was less in evidence this morning, but then on a Friday Chinese futures speculators (yes, there are some!) were probably closing positions before the weekend.

In other news, the ECB lowered its benchmark deposit rate by ¼% from 4%, the first of the majors to do so. Markets are buzzing with hope that the Fed and others will follow suite. But with budget deficits continuing to run high, inflation is far from over, and in the next few months we will see how funding them progresses, bearing in mind that immediate liquidity is drying up reflected in the US’s Reverse Repo position:

Most of this has gone into T-bills, funding the deficit and being spent on non-production. Liquidity is clearly running dry and higher borrowing costs beckon.

I think that any of the ' Technicians ' who carp on about Silver being at a much too high a level when set against the moving average's possibly need something of a wake up call . The conditions we are seeing right now per supply and demand differentials , the extent of the arbitrage between the

Comex / the LBMA and the SGE / SFE ( + 14 - 15% just recently ) , the massive under-reporting of industrial demand and off-take by China & India in particular , by the ' Silver Institute ' and the fact said demand for photovoltaics is ramping up exponentially where PV's and numerous other new application' where a substitute for Silver simply doesn't exist ........This is all completely unprecedented and form's the " Perfect Storm " in this market - something which you've alluded to any number of times and which has sunk in big time with a vast swathe of highly savvy Chinese savers . The question is just how long is it going to take for any of our fellow bretheren to finally wake up and smell the coffee as it were - possibly never or only when they catch a faint whiff of acrid diesel fumes as the Silver Train is disappearing up the line at an ever increasing lick ...??

" Wake Up & Smell the Coffee " ...etc - Coffee forecast likely to return to its all time high when it reached USD ' $ 3.11 a pound in 1977 ( at the moment $ 2.25 - $ 2.30 a pound ) , with this probably going to happen before the end of 2024 , and this being attributed crop cycles / poor harvest , and with no consideration of currency issues or exchange rates factored in ..etc .

" But with budget deficits continuing to run high , inflation is far from over " - potential winner of the top prize in the ' Understatement of the Year Competition '

Michael— Thanks for the link