Bond Armageddon ahead

The consequences of the Iran war are already driving weaker G7 bonds into multiyear higher yields. They will shape the future of all financial markets and of the currencies themselves.

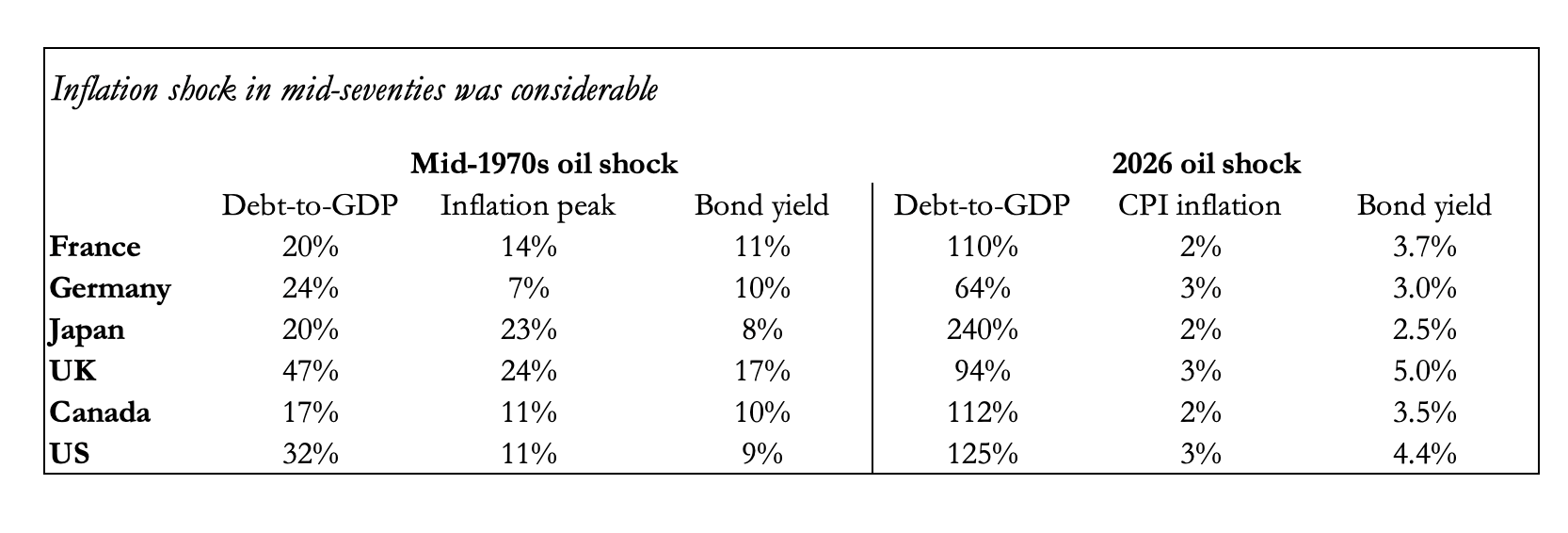

Markets are meant to discount the future by putting a price on it. But on the evidence, they are failing to do so as the table above intimates. Surely, we all know that the US attack on Iran has created a supply crisis in energy and its derivatives which will raise production costs of every consumer item. If these costs can’t be passed on to consumers, then businesses will go bust, creating mass unemployment.

Higher unemployment and loss of tax revenues destroy government revenues and increases welfare costs. Government finances are already in severe deficit. Yet, driven by Keynesian interventionism governments will be desperate to increase support of their private sectors and bail out consumers. But all that additional deficit spending will merely collapse G7 currencies’ purchasing power, driving price inflation into the mid-seventies’ outcome and probably even higher.

Already, financially challenged governments with record peace-time debt-to-GDPs are about to find their financial obligations go into hyperdrive. Yet, US treasury bond